LPA Safety Score

The LPA Safety Score (0–100) is the primary output of the /fund review-lpa command and the automated inbox review pipeline.

How It Works

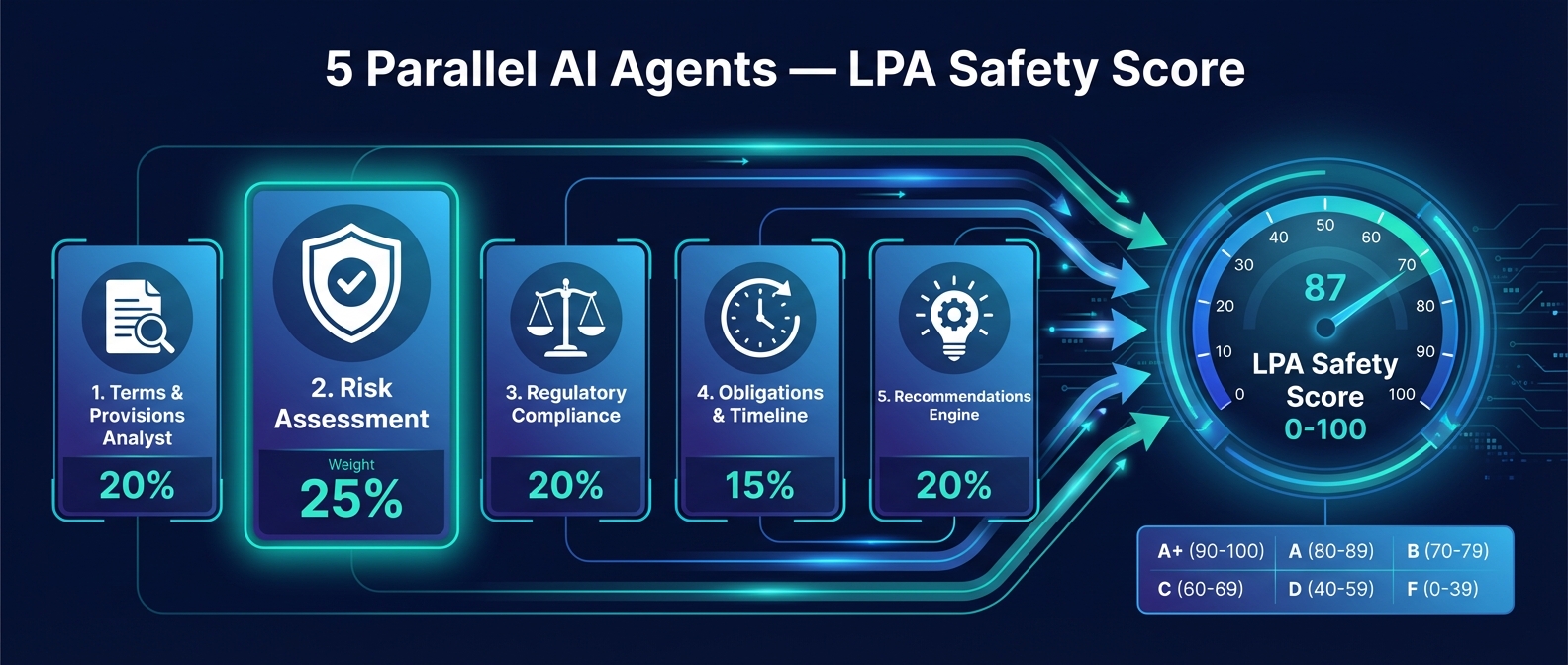

Five agents run in parallel, each analysing a different dimension of the LPA. Their scores are combined as a weighted average.

| Agent | Role | Weight |

|---|---|---|

fund-terms | Term extraction & categorisation | 20% |

fund-risks | Risk scoring (1–10 per provision) | 25% |

fund-compliance | Regulatory compliance checks | 20% |

fund-obligations | Obligations & timeline mapping | 15% |

fund-recommendations | Negotiation recommendations | 20% |

Agent data flows linearly: the Terms agent output feeds into Risk, Compliance, Obligations, and Recommendations agents.

Grade Thresholds

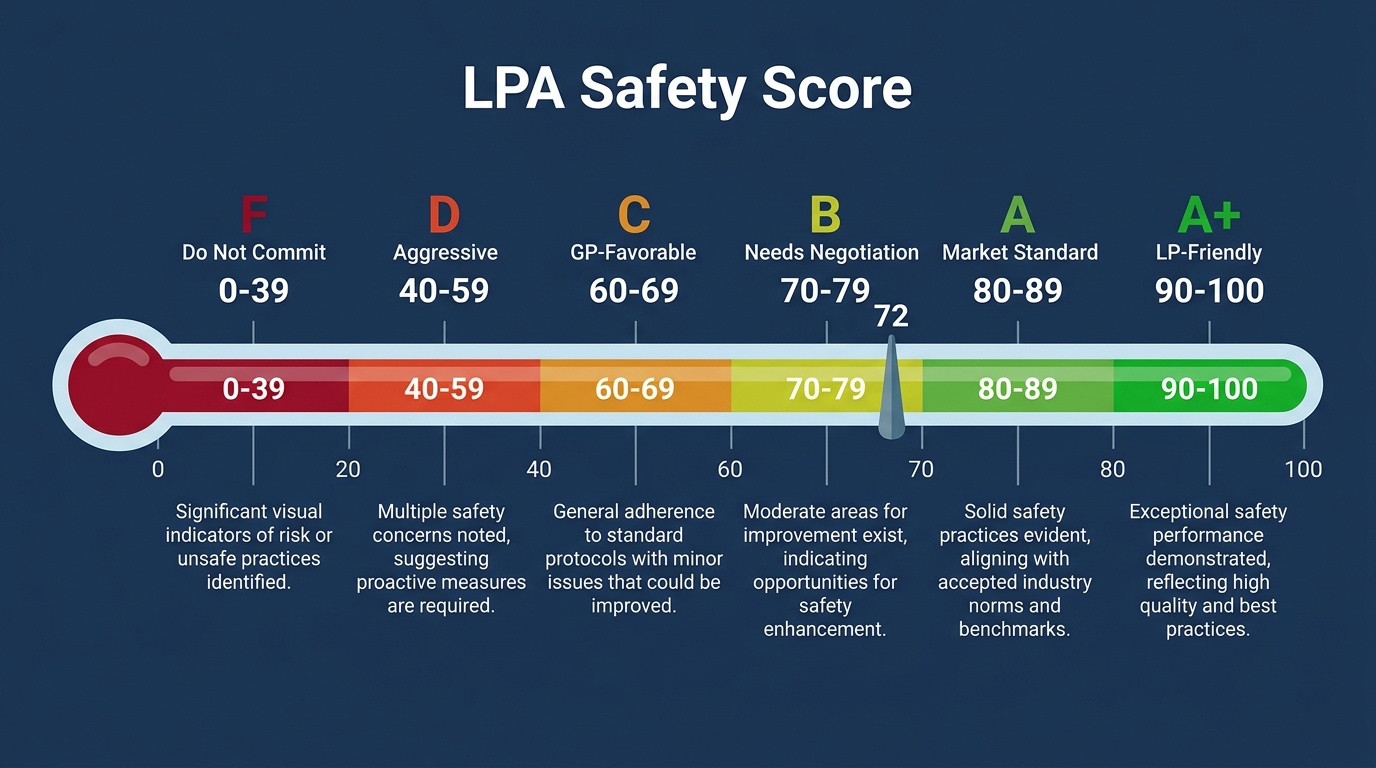

| Score | Grade | Interpretation |

|---|---|---|

| 90–100 | A | Investor-favourable, minor concerns only |

| 75–89 | B | Standard market terms with some negotiation points |

| 60–74 | C | Material issues, negotiation recommended |

| 45–59 | D | Significant risk, legal review required |

| 0–44 | F | Highly investor-unfavourable, do not sign without major revisions |

Implementation

The pipeline runs via the Anthropic SDK directly in apps/web/src/lib/review-pipeline.ts. It does not depend on the claude CLI binary.

PDF Prompt Caching

The document is sent once with cache_control: ephemeral. All five agent calls share the cached prefix, significantly reducing API cost for large documents.

Input Format

interface ReviewResult {

fundSlug: string;

fundName: string;

documentName: string;

reviewedAt: string;

safetyScore: number; // 0–100

grade: 'A' | 'B' | 'C' | 'D' | 'F';

verdict: string;

agents: AgentResult[];

totalFindings: number;

}Findings Severity

Each finding carries a severity level: high, med, or low. The compliance tracker raises macOS notifications for High Risk findings when running locally.

Triggering a Review

Via CLI (T1)

/fund review-lpa path/to/lpa.pdfVia Webapp Upload (T3)

Drop a PDF into the upload UI at /w/[slug]/upload. The inbox watcher picks it up within 30 seconds and triggers the pipeline automatically.

Via API (T3)

curl -X POST http://localhost:3000/api/review/trigger \

-H "Content-Type: application/json" \

-d '{"filename": "apex-lpa-2024.pdf", "fundId": "..."}'Via Direct Upload API

curl -X POST http://localhost:3000/api/upload \

-H "x-api-key: $UPLOAD_API_KEY" \

-F "file=@apex-lpa-2024.pdf"Intentional Test Issues

The sample LPA (generate_sample_lpa.py) contains 10 intentional issues for validating detection:

- Aggressive carry (25%, no hurdle)

- Weak clawback

- Broad GP discretion on investment period extension

- No LPAC consent for affiliate transactions

- Vague fee offsets

- Missing key person provision

- Overly broad confidentiality

- 120-day opt-out trap

- Free GP assignment

- No excuse/exclusion rights