Compliance Frameworks

FundAdmin AI's Regulatory Compliance agent checks every LPA against a comprehensive set of U.S. federal, European/international, and industry-standard regulatory frameworks. Compliance is not a spectrum -- a fund either meets the requirements of a framework or it does not. A single compliance failure can invalidate the fund structure, create personal liability for the GP, or expose LPs to unexpected tax withholding or regulatory action.

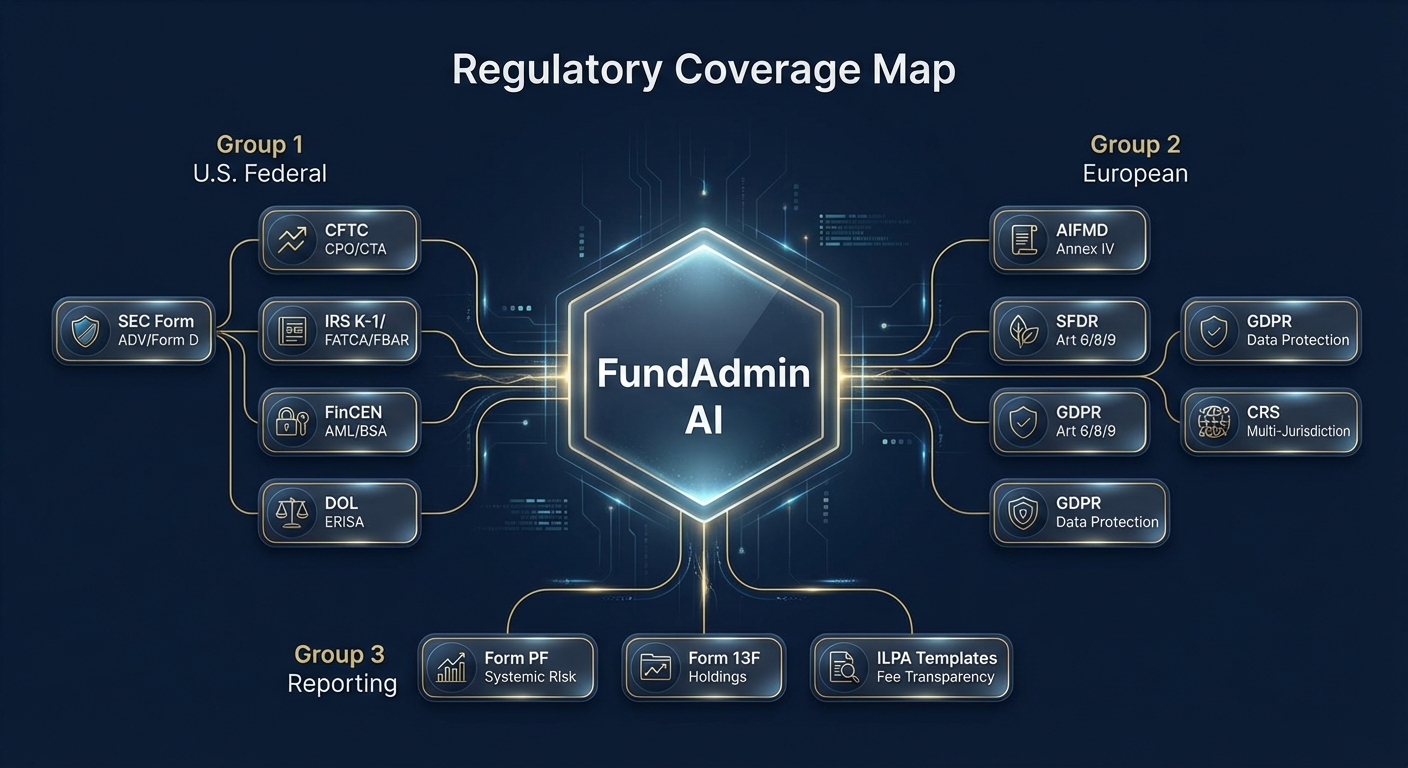

This page is a complete reference for every framework FundAdmin AI evaluates.

U.S. Federal Frameworks

SEC / Investment Advisers Act

What it is: The Investment Advisers Act of 1940 (as amended by Dodd-Frank) requires most fund managers to register with the SEC as investment advisers. Registration triggers ongoing disclosure, fiduciary, and compliance obligations.

What FundAdmin AI checks:

- Is the GP/adviser registered with the SEC? If not, is an exemption properly claimed (exempt reporting adviser, venture capital fund adviser, foreign private adviser)?

- Does the LPA reference Form ADV and make it available to investors?

- Are fiduciary obligations acknowledged in the LPA's standard of care and exculpation provisions?

- Is the annual Form ADV update obligation documented (must be updated within 90 days of fiscal year-end)?

Registration thresholds:

- $150M+ AUM: Must register (with limited exceptions)

- $25M-$150M: May register with SEC or state regulators depending on state rules

- Under $25M: Generally state-registered

- Exempt Reporting Adviser: Manages only qualifying private funds under $150M AUM; must still file abbreviated Form ADV

Key compliance risk: An unregistered adviser managing non-exempt funds faces enforcement action, potential fund unwinding, and personal liability. LPs investing with an unregistered, non-exempt adviser may face clawback of any preferential treatment.

Output: PASS / WARNING / FAIL

Form PF

What it is: Form PF (Private Fund) is a confidential reporting form filed with the SEC by registered investment advisers managing private funds. It provides systemic risk data to the Financial Stability Oversight Council (FSOC).

What FundAdmin AI checks:

- Does the fund's AUM trigger Form PF filing obligations?

- Is the filing frequency correct (quarterly vs annual)?

- Does the LPA acknowledge Form PF obligations and allocate filing costs appropriately?

- Are large fund reporting thresholds addressed for current-period event reporting?

Filing thresholds and frequency:

| Fund Type | Threshold | Filing Frequency | Deadline |

|---|---|---|---|

| Hedge funds (large) | $1.5B+ hedge fund AUM | Quarterly | 60 days after quarter-end |

| PE funds (large) | $2.0B+ PE fund AUM | Annually | 120 days after fiscal year-end |

| All other private fund advisers | $150M+ AUM | Annually | 120 days after fiscal year-end |

Large hedge fund current reporting: Since 2023 amendments, large hedge funds must also report certain triggering events (extraordinary investment losses, significant margin increases, large counterparty defaults, large withdrawal/redemption requests) within 72 hours.

Key compliance risk: Failure to file Form PF is an SEC enforcement matter. The more subtle risk is misclassifying fund type -- a fund that is technically a "hedge fund" under Form PF's broad definition but self-classifies as PE may miss quarterly filing obligations.

Output: PASS / WARNING / FAIL

Form D

What it is: Form D is a notice filing with the SEC required for securities offerings made under Regulation D (Rule 506(b) or 506(c)) -- the exemption most private funds rely on to avoid SEC registration of their securities.

What FundAdmin AI checks:

- Does the LPA reference the Reg D exemption being relied upon (506(b) or 506(c))?

- Is the Form D filing timeline documented (must be filed within 15 days of the first sale of securities)?

- Are amendment obligations addressed (material changes require an amended Form D)?

- For 506(c) offerings: is the general solicitation and verification of accredited investor status properly documented?

- Are blue sky (state) notice filing obligations addressed?

Key compliance risk: Failure to file Form D does not automatically disqualify the Reg D exemption, but the SEC considers it a factor in enforcement actions. More critically, some states condition their Reg D exemption on timely Form D filing and state notice filing -- missing the state deadline can create a state securities law violation.

Output: PASS / WARNING / FAIL

Form 13F

What it is: Form 13F requires institutional investment managers with $100M or more in qualifying securities to file quarterly reports of their holdings.

What FundAdmin AI checks:

- Does the fund or its adviser likely cross the $100M threshold in 13F securities?

- Is the Form 13F filing obligation acknowledged in the LPA or adviser's compliance manual?

- Are confidential treatment request procedures in place for sensitive positions?

Filing requirements:

- Threshold: $100M+ in Section 13(f) securities (generally U.S. exchange-traded equities and certain convertible securities)

- Frequency: Quarterly, within 45 days of quarter-end

- Content: Long positions in 13(f) securities; does not include short positions, options, or non-13(f) securities

Key compliance risk: For hedge funds and public equity funds, this is a routine filing. For PE and VC funds, 13F is rarely triggered because their holdings are private securities. FundAdmin AI flags this as informational when the fund strategy suggests public securities exposure.

Output: PASS / WARNING / N/A

ERISA

What it is: The Employee Retirement Income Security Act of 1974 governs retirement plans. When retirement plan assets (pension funds, 401(k) plans) invest in a private fund, the fund may become subject to ERISA's fiduciary, prohibited transaction, and reporting requirements -- unless an exemption applies.

What FundAdmin AI checks:

- Does the LPA include a 25% plan asset test provision?

- Is the fund relying on an operating company exemption (VCOC or REOC)?

- Are benefit plan investor limitations documented in the subscription agreement?

- Does the LPA restrict benefit plan investor participation to stay below the threshold?

The 25% Plan Asset Test:

A fund's assets are treated as "plan assets" (subject to ERISA) if 25% or more of any class of equity interests is held by benefit plan investors. The test is applied at each closing and at key subsequent dates.

Benefit Plan Investor Percentage =

(Commitments from Benefit Plan Investors) /

(Total Commitments - GP + Affiliates Commitments)If the fund crosses 25%, the GP becomes an ERISA fiduciary, prohibited transaction rules apply to every fund transaction, and compliance costs increase dramatically.

Operating Company Exemptions:

| Exemption | Requirement | Typical Fund Type |

|---|---|---|

| VCOC (Venture Capital Operating Company) | Fund must obtain management rights in at least 50% of its investments by value | PE, VC, growth equity |

| REOC (Real Estate Operating Company) | At least 50% of assets are real estate that the fund actively manages | Real estate |

If a VCOC or REOC exemption applies, the 25% test is irrelevant -- the fund is not treated as holding plan assets regardless of benefit plan investor participation.

Key compliance risk: Inadvertently crossing the 25% threshold without an operating company exemption converts the GP into an ERISA fiduciary overnight. This creates personal liability for the GP and potential prohibited transaction violations on every existing fund investment. This is one of the most consequential compliance failures in fund formation.

Output: PASS / WARNING / FAIL

AML / BSA / FinCEN

What it is: Anti-Money Laundering (AML) requirements under the Bank Secrecy Act (BSA), administered by the Financial Crimes Enforcement Network (FinCEN), require certain financial institutions to implement customer identification, due diligence, and suspicious activity reporting programs.

What FundAdmin AI checks:

- Does the subscription agreement include adequate KYC (Know Your Customer) procedures?

- Is beneficial ownership identification required for entity investors?

- Are OFAC (sanctions) screening procedures referenced?

- Does the LPA or subscription docs address the investor's obligation to provide accurate identity information?

- Are ongoing monitoring and SAR (Suspicious Activity Report) filing procedures acknowledged?

KYC Requirements:

| Investor Type | Required Information |

|---|---|

| Natural persons | Full legal name, date of birth, address, government ID number (SSN for U.S. persons) |

| Entities | Legal name, formation jurisdiction, principal place of business, EIN/tax ID |

| Beneficial owners | Identity of any individual owning 25%+ of the entity, plus one individual with significant management control |

| Trusts | Trustee identity, trust name, formation date, beneficiary information (if applicable) |

Sanctions Screening:

- All investors screened against OFAC's Specially Designated Nationals (SDN) list

- Screening at subscription and periodically thereafter

- Screening of beneficial owners, not just the investing entity

Key compliance risk: AML violations carry criminal penalties. A fund that accepts an investment from a sanctioned person or entity faces asset freezing, substantial fines, and criminal prosecution of responsible individuals. Even negligent failure to screen is prosecutable.

Output: PASS / WARNING / FAIL

FATCA

What it is: The Foreign Account Tax Compliance Act requires foreign financial institutions (FFIs) to report U.S. person accounts to the IRS, and requires U.S. withholding agents to withhold 30% on certain payments to non-compliant FFIs. Private funds are generally withholding agents and may also be FFIs.

What FundAdmin AI checks:

- Does the subscription agreement require W-8 (non-U.S. investors) and W-9 (U.S. investors) collection?

- Is the fund's entity classification properly documented (FFI, NFFE, deemed-compliant FFI)?

- Are Chapter 4 withholding obligations addressed in the LPA?

- Does the LPA give the GP authority to withhold and remit taxes on behalf of non-compliant investors?

- Are intergovernmental agreement (IGA) considerations addressed for non-U.S. feeder structures?

Entity Classification:

| Classification | Description | FATCA Obligation |

|---|---|---|

| FFI (Foreign Financial Institution) | Non-U.S. entity that accepts deposits, holds financial assets, or is an investment entity | Must register with IRS, obtain GIIN, report U.S. accounts |

| NFFE (Non-Financial Foreign Entity) | Non-U.S. entity that does not meet FFI criteria | Must certify substantial U.S. owner status on W-8BEN-E |

| Deemed-Compliant FFI | FFI that meets requirements for deemed compliance (e.g., local FFI, restricted fund) | Reduced reporting obligations |

| Participating FFI | FFI that has entered an FFI agreement with the IRS | Full reporting and withholding obligations |

W-Form Collection:

| Form | Who Completes | Purpose |

|---|---|---|

| W-9 | U.S. persons (individuals and entities) | Certify TIN and exemption status |

| W-8BEN | Non-U.S. individuals | Claim treaty benefits, certify foreign status |

| W-8BEN-E | Non-U.S. entities | Certify entity classification, claim treaty benefits, FATCA status |

| W-8IMY | Non-U.S. intermediaries | Certify intermediary status for flow-through withholding |

Key compliance risk: Failure to properly collect W-forms and classify entities results in mandatory 30% withholding on withholdable payments. For a fund distributing $100M, improper FATCA compliance can mean $30M in unnecessary withholding that may take years to recover.

Output: PASS / WARNING / FAIL

European / International Frameworks

AIFMD (Alternative Investment Fund Managers Directive)

What it is: The EU's regulatory framework for alternative investment fund managers (AIFMs). AIFMD imposes authorization, transparency, reporting, and investor protection requirements on managers of alternative investment funds marketed in the EU.

What FundAdmin AI checks:

- If the fund is marketed to EU investors, is AIFMD compliance addressed?

- Is Annex IV reporting referenced (semi-annual or annual regulatory reporting)?

- Are leverage disclosures included (commitment method and gross method calculations)?

- Is a depositary appointed as required for EU-marketed funds?

- Are national private placement regime (NPPR) requirements addressed for non-EU managers marketing into the EU?

- Is the AIFM remuneration policy disclosed?

Annex IV Reporting:

Annex IV is a standardized regulatory report filed by AIFMs with their home-state regulator. It includes:

- AUM and NAV

- Investment strategy and geographic/sector exposure

- Leverage ratios (commitment method and gross method)

- Liquidity profile

- Risk profile (market, credit, counterparty, liquidity, operational)

- Stress test results

Filing frequency depends on AUM:

- Under EUR 100M (unleveraged) or EUR 500M (leveraged): Annual

- EUR 500M-1B: Semi-annual

- Over EUR 1B: Quarterly

Depositary Requirements:

- EU-managed AIFs must appoint a depositary (custodian) in the AIF's home state

- The depositary monitors cash flows, safekeeps assets, and provides oversight of NAV calculation

- Non-EU managers using NPPR may have modified depositary requirements depending on the member state

Key compliance risk: Marketing a fund in the EU without AIFMD compliance (either through full authorization or NPPR) constitutes a regulatory violation in every member state where marketing occurs. Penalties vary by jurisdiction but can include fines and prohibition on future marketing.

Output: PASS / WARNING / FAIL / N/A

SFDR (Sustainable Finance Disclosure Regulation)

What it is: The EU regulation requiring financial market participants (including AIFMs) to make sustainability-related disclosures at both the entity level and the product (fund) level.

What FundAdmin AI checks:

- Is the fund classified under Article 6 (no sustainability objective), Article 8 (promotes environmental/social characteristics), or Article 9 (sustainable investment objective)?

- Are the 18 mandatory Principal Adverse Impact (PAI) indicators addressed?

- Is pre-contractual disclosure (Annex II for Article 8, Annex III for Article 9) included or referenced?

- Are website disclosure obligations addressed?

- Is periodic reporting (annual PAI statement) referenced?

Article Classification:

| Article | Description | Disclosure Obligation |

|---|---|---|

| Article 6 | Fund does not promote ESG characteristics or have a sustainability objective | Must disclose how sustainability risks are integrated (or explain why not) |

| Article 8 | Fund promotes environmental or social characteristics | Must disclose promoted characteristics, how they are met, benchmark index (if any), and PAI consideration |

| Article 9 | Fund has sustainable investment as its objective | Must disclose sustainable investment objective, no significant harm assessment, and alignment with EU Taxonomy |

18 Mandatory PAI Indicators (for entities that consider adverse impacts):

- GHG emissions (Scope 1, 2, 3)

- Carbon footprint

- GHG intensity of investee companies

- Exposure to fossil fuel companies

- Non-renewable energy share (consumption and production)

- Energy consumption intensity per high-impact sector

- Activities negatively affecting biodiversity-sensitive areas

- Emissions to water

- Hazardous waste and radioactive waste ratio

- Violations of UN Global Compact / OECD Guidelines

- Lack of processes and compliance mechanisms to monitor UN GC / OECD

- Unadjusted gender pay gap

- Board gender diversity

- Exposure to controversial weapons

- GHG intensity (sovereign)

- Countries subject to social violations (sovereign)

- Exposure to real estate assets with poor energy efficiency

- Additional indicators (entity must select at least one additional from Annex I)

Key compliance risk: SFDR misclassification is a growing enforcement focus. Labeling a fund as Article 8 without adequate substantiation ("greenwashing") exposes the manager to regulatory action, investor litigation, and reputational damage. FundAdmin AI flags classification inconsistencies between the LPA's stated strategy and its SFDR disclosure.

Output: PASS / WARNING / FAIL / N/A

CRS (Common Reporting Standard)

What it is: The OECD's multilateral framework for automatic exchange of financial account information between tax jurisdictions. Over 100 jurisdictions participate. CRS is the international equivalent of FATCA.

What FundAdmin AI checks:

- Does the subscription agreement require self-certification from all investors regarding their tax residency?

- Are reportable jurisdiction identification procedures in place?

- Is the fund (or its administrator) registered for CRS reporting in each applicable jurisdiction?

- Are annual CRS reporting deadlines tracked?

- Does the LPA address the fund's obligation to report account balances, income, and gross proceeds to relevant tax authorities?

Self-Certification Requirements:

Every investor must provide a self-certification form documenting:

- Legal name

- Address

- Jurisdiction(s) of tax residence

- Taxpayer identification number(s) in each jurisdiction

- Entity type classification (financial institution, active NFE, passive NFE)

- Controlling persons (for passive NFEs -- individuals who control the entity)

Multi-Jurisdiction Reporting:

A fund with investors from multiple CRS jurisdictions must report account information to each investor's jurisdiction of tax residence through the fund's own jurisdiction of registration. For example, a Cayman Islands fund with a UK tax-resident investor reports the UK investor's information to the Cayman Islands Tax Information Authority, which exchanges it with HMRC.

Key compliance risk: Failure to collect self-certifications results in the investor being treated as reportable to all CRS jurisdictions -- maximum reporting exposure. Failure to report entirely can result in penalties from the fund's jurisdiction of registration and potential sanctions by exchange partner jurisdictions.

Output: PASS / WARNING / FAIL / N/A

GDPR (General Data Protection Regulation)

What it is: The EU regulation governing the processing of personal data of individuals in the EU/EEA. Private funds process significant personal data -- investor names, addresses, tax IDs, bank details, beneficial ownership information -- and must comply with GDPR when that data relates to EU/EEA individuals.

What FundAdmin AI checks:

- Does the LPA or subscription agreement include a data protection notice for EU/EEA investors?

- Is the lawful basis for processing investor data identified (legitimate interest, contractual necessity, legal obligation)?

- Are data subject rights acknowledged (access, rectification, erasure, portability, restriction, objection)?

- Is a Data Protection Officer (DPO) appointed (if required)?

- Are cross-border data transfer mechanisms documented for transfers outside the EEA (Standard Contractual Clauses, adequacy decisions)?

- Is a data processing agreement in place with service providers (administrators, auditors, legal counsel) who process investor personal data?

Personal Data Processed by Funds:

| Data Category | Examples | GDPR Basis |

|---|---|---|

| Identity data | Name, address, date of birth, nationality | Contractual necessity / Legal obligation (KYC) |

| Financial data | Bank details, capital account balances, distributions | Contractual necessity |

| Tax data | Tax ID, tax residency, W-8/W-9 forms | Legal obligation (FATCA, CRS) |

| Beneficial ownership | UBO names, ownership percentages | Legal obligation (AML) |

| Communication data | Email, phone, correspondence | Legitimate interest |

Key compliance risk: GDPR fines can reach EUR 20 million or 4% of annual global turnover (whichever is higher). For fund managers, the more practical risk is investor complaints to data protection authorities, which trigger investigations and reputational damage. Ensuring proper notices, lawful bases, and data processing agreements are in place is foundational.

Output: PASS / WARNING / FAIL / N/A

Industry Standards

ILPA (Institutional Limited Partners Association)

What it is: ILPA is the industry body representing institutional LPs. It publishes best practice guidelines, model LPA provisions, standardized reporting templates, and due diligence questionnaire (DDQ) templates that define what "market standard" means from the LP perspective.

What FundAdmin AI checks:

- Does the fund's fee reporting align with the ILPA Fee Reporting Template?

- Are all fee and expense categories disclosed with adequate granularity?

- Is the management fee calculation methodology transparent?

- Are portfolio company fee offsets documented?

- Does the LPA address items in the ILPA Principles (current version 3.0)?

- Alignment of interest (GP commitment, co-investment, clawback)

- Governance (LPAC, removal rights, key person)

- Transparency (reporting, fee disclosure, valuation)

- Is the fund's DDQ (Due Diligence Questionnaire) consistent with ILPA's template?

- Firm overview, investment strategy, team, track record

- Terms and structure

- Operations and compliance

- ESG integration

ILPA Principles 3.0 Key Provisions:

| Principle | ILPA Standard | What to Look For |

|---|---|---|

| GP Commitment | Meaningful cash commitment (not fee waiver) | 2-5% of fund size in cash |

| Management Fee | Transparent, market-rate, with post-investment step-down | Step-down to invested capital basis |

| Fee Offset | 100% offset of all portfolio company fees | At least 80% offset |

| Carried Interest | Whole-fund (European) waterfall preferred | European > American |

| Clawback | Personal, joint and several, with escrow | 25-30% escrow |

| LPAC | Independent, with authority over conflicts and extensions | Meaningful consent rights |

| Key Person | Named, with investment period suspension | Clear trigger and consequence |

| Reporting | Quarterly, with ILPA-compliant fee reporting | Within 60 days of quarter-end |

| Valuation | Independent valuation policy, annual audit | Third-party valuation for material positions |

Key compliance risk: ILPA standards are not legally binding, but deviation from ILPA best practices signals GP-unfriendly terms to sophisticated institutional investors. LPs increasingly use ILPA compliance as a threshold screen -- funds that deviate substantially may be excluded from consideration.

Output: PASS / WARNING / FAIL

SOC 1 / SOC 2

What it is: System and Organization Controls (SOC) reports, issued under AICPA standards, provide assurance over a service organization's internal controls. SOC 1 focuses on controls relevant to financial reporting; SOC 2 focuses on security, availability, processing integrity, confidentiality, and privacy.

What FundAdmin AI checks:

- Does the LPA require the fund administrator to maintain a SOC 1 report (relevant for NAV calculation, capital account maintenance, and investor reporting)?

- Is a SOC 2 report required for technology service providers handling investor data?

- Are SOC report review obligations included in the GP's operational procedures?

- Is the SOC report type specified (Type I = design only; Type II = design and operating effectiveness over a period)?

SOC Report Types:

| Report | Focus | Who Needs It | Type I vs Type II |

|---|---|---|---|

| SOC 1 | Financial reporting controls | Fund administrators processing NAV, capital calls, distributions | Type II preferred (covers operating effectiveness over 6-12 months) |

| SOC 2 | Security, availability, confidentiality, privacy, processing integrity | Technology platforms, cloud providers, data warehouses | Type II preferred |

What LPs Should Expect:

- Fund administrator: SOC 1 Type II report, covering NAV calculation, capital call processing, distribution processing, investor reporting, and reconciliation controls

- Technology platforms (investor portal, document management): SOC 2 Type II report

- The GP should review SOC reports annually and address any noted exceptions

Key compliance risk: SOC reports are not regulatory requirements, but institutional investors and their auditors increasingly require them. A fund administrator without a SOC 1 report creates audit friction for every LP, because the LP's auditor cannot rely on the administrator's controls and must perform additional testing. This is an operational risk that flows through to LP satisfaction and retention.

Output: PASS / WARNING / N/A

How Compliance Scoring Works

Framework Applicability

Not every framework applies to every fund. FundAdmin AI first determines which frameworks are applicable based on:

- Fund domicile: A Cayman Islands fund does not need to comply with AIFMD unless marketed in the EU

- Investor base: ERISA only applies if benefit plan investors participate; GDPR only applies if EU persons are involved

- Fund type: Form 13F is relevant for public equity strategies, not PE/VC

- Manager registration: Form PF obligations depend on adviser registration status and AUM

Non-applicable frameworks are marked N/A and do not affect the Safety Score.

Impact on Safety Score

Compliance findings affect the Safety Score through the Regulatory Compliance agent (20% weight):

| Finding | Score Impact |

|---|---|

| All applicable frameworks PASS | Agent scores 90-100 |

| One or more WARNINGs, no FAILs | Agent scores 70-89 depending on severity |

| One FAIL in a non-critical framework | Agent scores 50-69 |

| One FAIL in a critical framework (SEC, ERISA, AML) | Agent scores 30-49 |

| Multiple FAILs in critical frameworks | Agent scores 0-29 |

Because the Compliance agent carries 20% of the total Safety Score, a FAIL in a critical framework can reduce the composite score by 10-15 points -- enough to drop a fund from B to C or C to D grade.

Cross-Agent Interaction

Compliance findings also influence other agents:

- A FAIL on ERISA triggers a P0 (Dealbreaker) recommendation from the Recommendations Engine

- A WARNING on AML/KYC triggers additional risk scoring from the Risk Assessment agent on operational risk

- Missing compliance provisions (e.g., no FATCA withholding authority) create gaps in the Terms agent's completeness scores

This cross-agent interaction ensures that compliance failures are not siloed -- they ripple through the entire analysis and are reflected in the composite Safety Score, the risk dashboard, and the prioritized recommendation list.

Investor Compliance Skills

Beyond LPA-level compliance checks, FundAdmin AI includes six dedicated investor compliance skills that operate at the individual investor level. These skills implement the full subscription pipeline:

investor-classify → suitability-check → fatca-crs-classify → aml-screen → kyc-tracker → subscription-processinvestor-classify

Classifies each investor into one of ten investor types:

| Type | Examples |

|---|---|

| U.S. Individual | Natural persons, joint accounts |

| U.S. Entity | LLCs, LPs, corporations, trusts |

| Tax-Exempt | Endowments, foundations, pension funds |

| Benefit Plan | ERISA plans, 401(k), IRA |

| Government | Sovereign wealth funds, public pension |

| Non-U.S. Individual | Foreign natural persons |

| Non-U.S. Entity | Foreign corporations, foreign partnerships |

| Financial Institution | Banks, broker-dealers, insurance companies |

| Fund-of-Funds | Other investment funds |

| Special | Feeder funds, SPVs, blocker entities |

Classification drives all downstream compliance requirements: which suitability thresholds apply, which FATCA forms to collect, whether ERISA monitoring is needed, and which AML/KYC procedures to follow.

suitability-check

Verifies investor qualification against three threshold levels -- Accredited Investor, Qualified Client, and Qualified Purchaser -- using the thresholds defined in the LPA and the fund's exemption structure. Flags investors who do not meet the required qualification level for the fund's Reg D exemption.

fatca-crs-classify

Determines the investor's FATCA entity classification (FFI, NFFE, deemed-compliant FFI) and CRS self-certification requirements. Identifies which W-forms to collect (W-9, W-8BEN, W-8BEN-E, W-8IMY) and which CRS reporting jurisdictions apply. Cross-validates collected forms against the investor's stated classification.

aml-screen

Runs AML screening on the investor and all beneficial owners (individuals owning 25%+ of the investing entity). Checks against OFAC SDN list, FinCEN advisories, and PEP (Politically Exposed Person) databases. Generates a screening report with match results and risk flags.

kyc-tracker

Tracks KYC status for every investor across the fund lifecycle. Maintains a KYC record with document collection status, expiration dates, and refresh requirements. Standard refresh cycles:

| Investor Risk Level | KYC Refresh |

|---|---|

| Low risk | Every 3 years |

| Medium risk | Every 2 years |

| High risk / PEP | Annually |

The KYC Tracker integrates with the Obsidian vault's KYC Status dashboard, surfacing upcoming expirations and overdue reviews in the Action Items board.

subscription-process

Orchestrates the full subscription pipeline as a single command. Accepts a completed subscription document, runs all five upstream checks in sequence, and produces a consolidated subscriber report with a pass/fail decision and a list of any outstanding items. Investors who pass all checks are marked ready for GP acceptance; investors with open items are flagged for follow-up.

See Investor Onboarding for a complete walkthrough of the subscription pipeline.